SLIDE 1

Applied Econometrics with R

Christian Kleiber Universit¨ at Basel Switzerland Achim Zeileis Wirtschaftsuniversit¨ at Wien Austria

Outline

- R and econometrics

- Robust standard errors

Example: Sandwich variance estimators for a tobit model

- Gaps

- AER: book and package

Christian Kleiber

1

U Basel

R and econometrics

- Language and terminology in econometrics is somewhat distinct from the terminol-

- gy used in mainstream statistics.

Two examples: Statistics Econometrics factor dummy variables generalized linear model probit, logit, ...

- Generally, not much awareness of statistical GLM literature among econometricians.

- Visualization not very common.

Christian Kleiber

2

U Basel

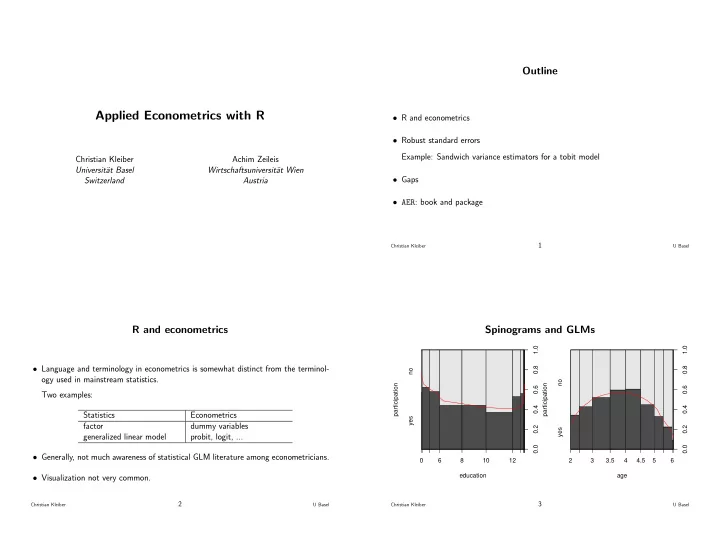

Spinograms and GLMs

education participation 6 8 10 12 yes no 0.0 0.2 0.4 0.6 0.8 1.0 age participation 2 3 3.5 4 4.5 5 6 yes no 0.0 0.2 0.4 0.6 0.8 1.0

Christian Kleiber

3

U Basel