SLIDE 1

AUG 26 TH , 2020 JAGUAR MEDIA CHINESE TECH DEMYSTIFIED SERIES - - PDF document

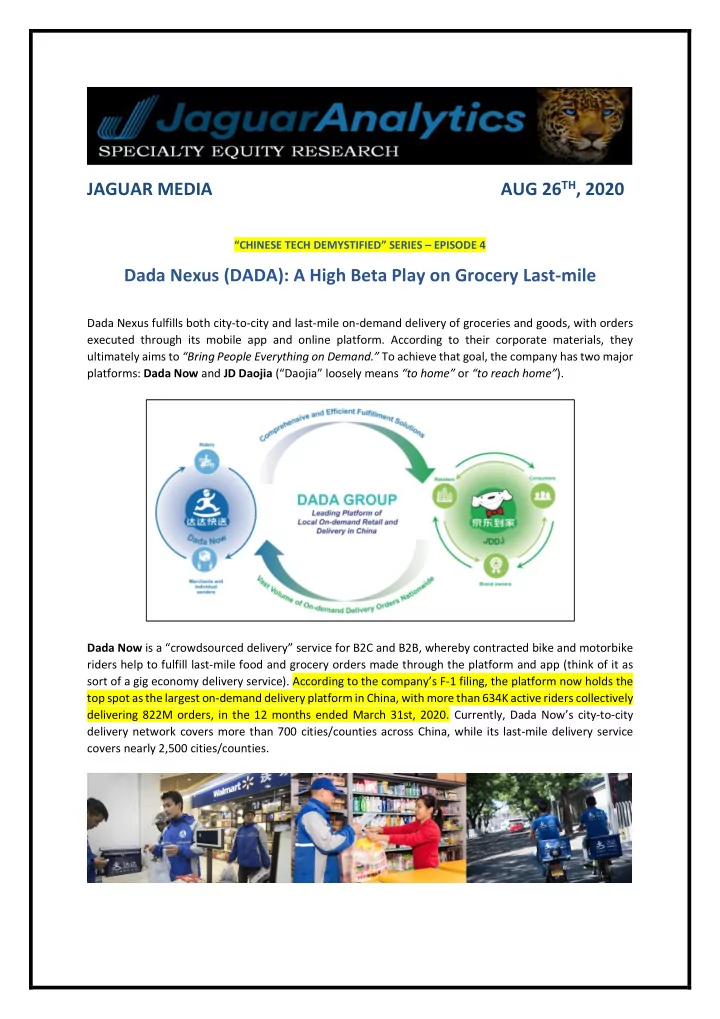

AUG 26 TH , 2020 JAGUAR MEDIA CHINESE TECH DEMYSTIFIED SERIES EPISODE 4 Dada Nexus (DADA): A High Beta Play on Grocery Last-mile Dada Nexus fulfills both city-to-city and last-mile on-demand delivery of groceries and goods, with orders