Markets are trying to digest the political and economic ramifications of the surprise result of the UK referendum on EU membership. The vote to leave was arguably one of the UK’s most important political decisions of the past 60 years, and will have deep and profound political and economic implications. The negative impact on equity markets and sterling was immediate, as was the change in the UK’s political

- leadership. Markets remain volatile given the uncertainty over the potential timing and terms of a managed UK

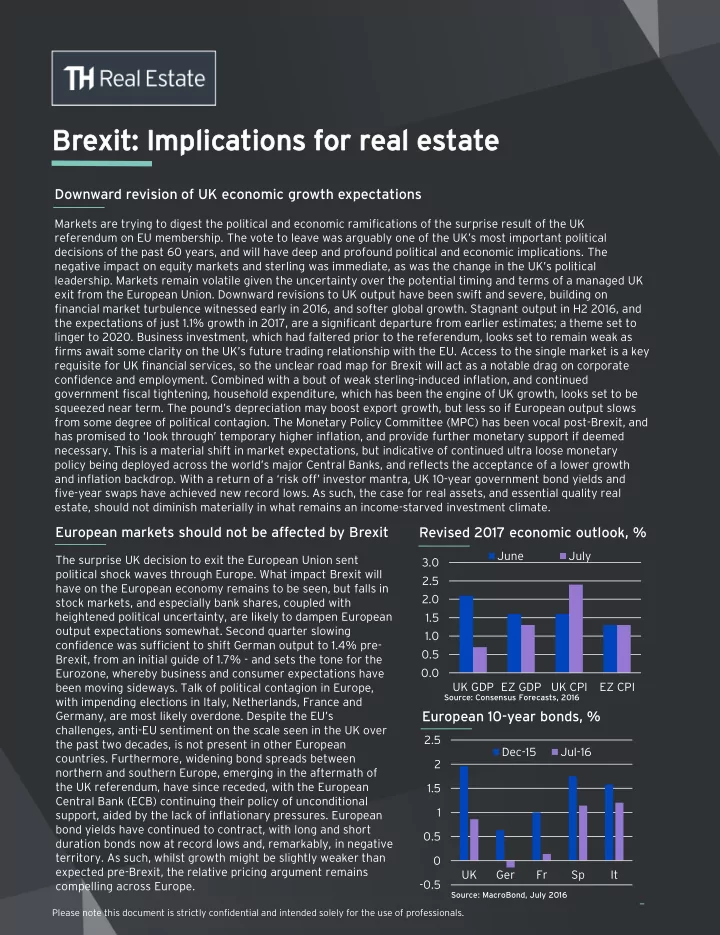

exit from the European Union. Downward revisions to UK output have been swift and severe, building on financial market turbulence witnessed early in 2016, and softer global growth. Stagnant output in H2 2016, and the expectations of just 1.1% growth in 2017, are a significant departure from earlier estimates; a theme set to linger to 2020. Business investment, which had faltered prior to the referendum, looks set to remain weak as firms await some clarity on the UK’s future trading relationship with the EU. Access to the single market is a key requisite for UK financial services, so the unclear road map for Brexit will act as a notable drag on corporate confidence and employment. Combined with a bout of weak sterling-induced inflation, and continued government fiscal tightening, household expenditure, which has been the engine of UK growth, looks set to be squeezed near term. The pound’s depreciation may boost export growth, but less so if European output slows from some degree of political contagion. The Monetary Policy Committee (MPC) has been vocal post-Brexit, and has promised to ‘look through’ temporary higher inflation, and provide further monetary support if deemed

- necessary. This is a material shift in market expectations, but indicative of continued ultra loose monetary

policy being deployed across the world’s major Central Banks, and reflects the acceptance of a lower growth and inflation backdrop. With a return of a ‘risk off’ investor mantra, UK 10-year government bond yields and five-year swaps have achieved new record lows. As such, the case for real assets, and essential quality real estate, should not diminish materially in what remains an income-starved investment climate.

Brexit xit: : Implicatio ations ns for rea eal l estate

European markets should not be affected by Brexit

Please note this document is strictly confidential and intended solely for the use of professionals.

The surprise UK decision to exit the European Union sent political shock waves through Europe. What impact Brexit will have on the European economy remains to be seen, but falls in stock markets, and especially bank shares, coupled with heightened political uncertainty, are likely to dampen European

- utput expectations somewhat. Second quarter slowing

confidence was sufficient to shift German output to 1.4% pre- Brexit, from an initial guide of 1.7% - and sets the tone for the Eurozone, whereby business and consumer expectations have been moving sideways. Talk of political contagion in Europe, with impending elections in Italy, Netherlands, France and Germany, are most likely overdone. Despite the EU’s challenges, anti-EU sentiment on the scale seen in the UK over the past two decades, is not present in other European

- countries. Furthermore, widening bond spreads between

northern and southern Europe, emerging in the aftermath of the UK referendum, have since receded, with the European Central Bank (ECB) continuing their policy of unconditional support, aided by the lack of inflationary pressures. European bond yields have continued to contract, with long and short duration bonds now at record lows and, remarkably, in negative

- territory. As such, whilst growth might be slightly weaker than

expected pre-Brexit, the relative pricing argument remains compelling across Europe.

Downward revision of UK economic growth expectations

0.0 0.5 1.0 1.5 2.0 2.5 3.0 UK GDP EZ GDP UK CPI EZ CPI June July

Revised 2017 economic outlook, %

- 0.5

0.5 1 1.5 2 2.5 UK Ger Fr Sp It Dec-15 Jul-16

European 10-year bonds, %

Source: Consensus Forecasts, 2016 Source: MacroBond, July 2016