SLIDE 20 20

Media Statement

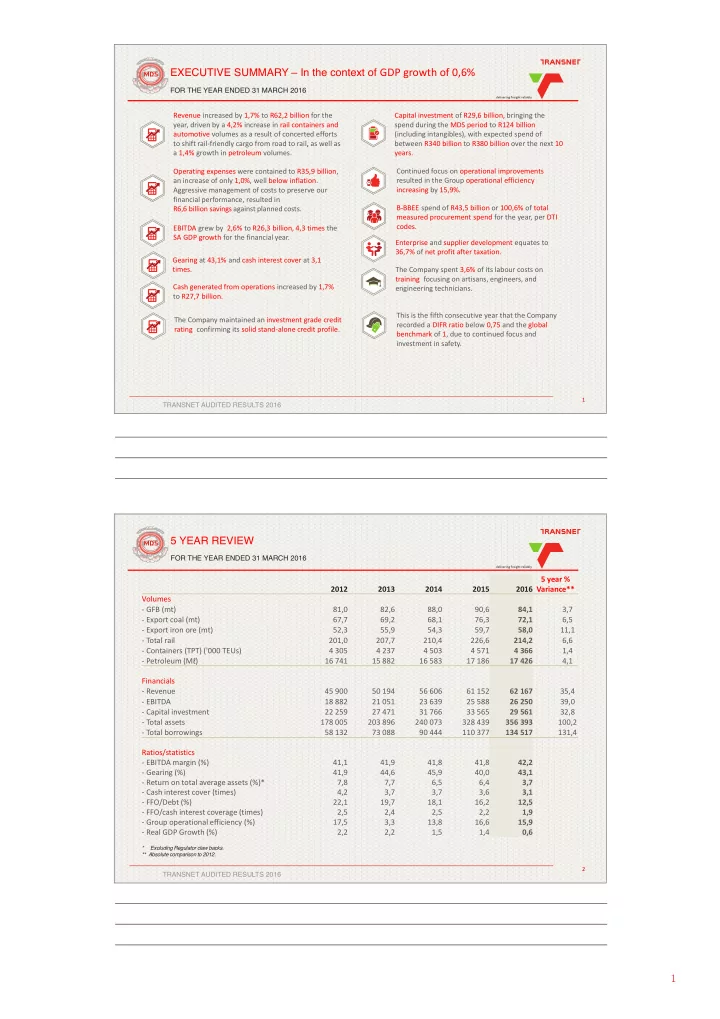

Transnet posts solid results amid harsh economic environment Company maintains record level of capital expenditure, posts EBITDA growth well in excess of GDP growth.

Highlights

- Revenue up 1,7% to R62,2 billion.

- Operating costs contained at a modest increase of 1% to

R35,9 billion.

- EBITDA grew by 2,6% to R26,3 billion, 4,3 times GDP

growth of 0,6%.

- Capital investment of R29,6 billion, bringing the spend

during the MDS period to R124 billion.

- Capital programme revised upwards to R340 billion-

R380 billion over the next 10 years.

- Cash generated from operations increased by 1,7% to

R27,7 billion.

- Gearing at 43,1% and cash interest cover at 3,1 times.

- Group operational effjciency increased by 15,9%.

- Maintained an investment grade credit rating, confjrming

the company’s standalone credit profjle.

- B-BBEE spend of R43,5 billion or 100,6% of total measured

procurement spend for the year, per DTI codes. Transnet today unveiled a positive set of results for the year ended 31 March 2016. This was despite a tough economic environment characterised by weak economic activity which undermined growth in volumes across most commodities and freight businesses. Revenue for the year increased by 1,7% to R62,2 billion underpinned by a 4,2% increase in rail containers and automotive volumes to 14,9 million tonnes (mt), from 14,3mt in the previous year, while petroleum volumes increased by 1,4% to 17,4 billion

- litres. This is testament to the strides that the company is

making in gaining market share and moving rail-friendly cargo

Revenue from cross-border activities increased from R1,5 billion to R2,8 billion as the company’s plans to expand into the rest of the African continent gather momentum. However, the uncertain economic environment, combined with depressed commodity prices resulted in customers downscaling

- perations, which led to a 5,5% decrease in total rail volumes to

214,2mt, from 226,6mt in the previous year. Coal export volumes decreased by 5,5% to 72,1mt (2015:76,3mt), while iron ore export volumes fell 3% to 58mt compared to the previous year (2015: 59,7mt). Manganese volumes were fmat at 9,6mt. Encouragingly, Group operational effjciency increased by 15,9%. Both on-time departures and on-time arrivals in the general freight business improved signifjcantly compared to the previous

- year. This is as a result of continuous en-route monitoring of the

mainline trains. Transnet Port Terminals, the port operations division, recorded a substantial increase in effjciency levels across its terminals as efforts to turn vessels around faster began to pay off. The Ngqura Container Terminal showed the most signifjcant progress, with average moves per ship working hour (SWH) – an internationally recognised measure of terminal productivity – advancing from 48 to 66 moves. Durban Container Terminal’s Pier 1 improved from 48 to 53 moves, Pier 2 recorded an increase from 58 to 63 moves, while Cape Town Container Terminal improved from 49 to 53 moves. To mitigate the impact of slow growth, the company implemented various cost-containment measures, including stringent management of overtime, reducing the engagement

- f consultants and imposing a limit on discretionary costs.

Operating costs went up by a modest 1%, well below infmation, to R35,9 billion (2015: R35,6 billion) despite an increase in personnel and electricity costs. The cost-containment drive yielded R6,6 billion savings against planned costs. As a result, Transnet’s key measure of profjtability, earnings before interest, taxation, depreciation and amortisation (EBITDA) ) increased by 2,6% to R26,3 billion compared with R25,6 billion in the previous year, well in excess of GDP growth of 0,6% and a sector specifjc contraction of 0,1%. Encouragingly, and in line with our ground-breaking counter cyclical infrastructure investment programme under the Market Demand Strategy (MDS), the company sustained its commitment to the modernisation and renewal of the country’s transport and logistics infrastructure, spending R29,6 billion during the

- year. This took the total spend since the launch of the MDS to

an unprecedented R124 billion. The global economic slowdown has resulted in key customers deferring their expansion

- programmes. Transnet is committed to investing in an optimised

capital portfolio that is responsive to validated demand. The company plans to invest R340 billion-R380 billion over the next 10 years. This is likely to take the MDS spend to a record half a trillion rand of investment. The company’s most recent locomotive acquisition programme which resulted in the purchase of 1 319 new locomotives for the General Freight and Coal businesses, remains on track. By year- end, Transnet had spent R8,8 billion on the programme, taking

- verall spend to R26,3 billion thus far. In addition, 95 Class 20

electric locomotives, 100 Class 21 electric locomotives and 60 Class 43 diesel locomotives were delivered and accepted into

- perations. This has allowed Transnet to phase out some of the

40 year old aging locomotive fmeet. Other capital investment highlights include:

- R2,3 billion spent on 2 100 wagons that have been delivered

to Freight Rail.

- R1,3 billion invested in the New Multi-Product Pipeline.

- R4 billion invested mainly on the maintenance and

acquisition of cranes, dredgers, tugs and straddle carriers.

- R256 million has been invested in the coal line expansion for

upgrading yards, lines and electrical equipment. Transnet’s capital investment programme is supported by a Board-approved funding strategy. Despite persistent adverse market conditions, Transnet remained an attractive investment destination during the year. As a result, the company raised R40,9 billion, without government guarantees, through various sources, including:

- R8,3 billion from development fjnance institutions;

- R8,5 billion of commercial paper and call loans;

- R19,1 billion of domestic bank and club loans; and

- R4,6 billion of domestic bond issues.