SLIDE 1

11/9/2017 1

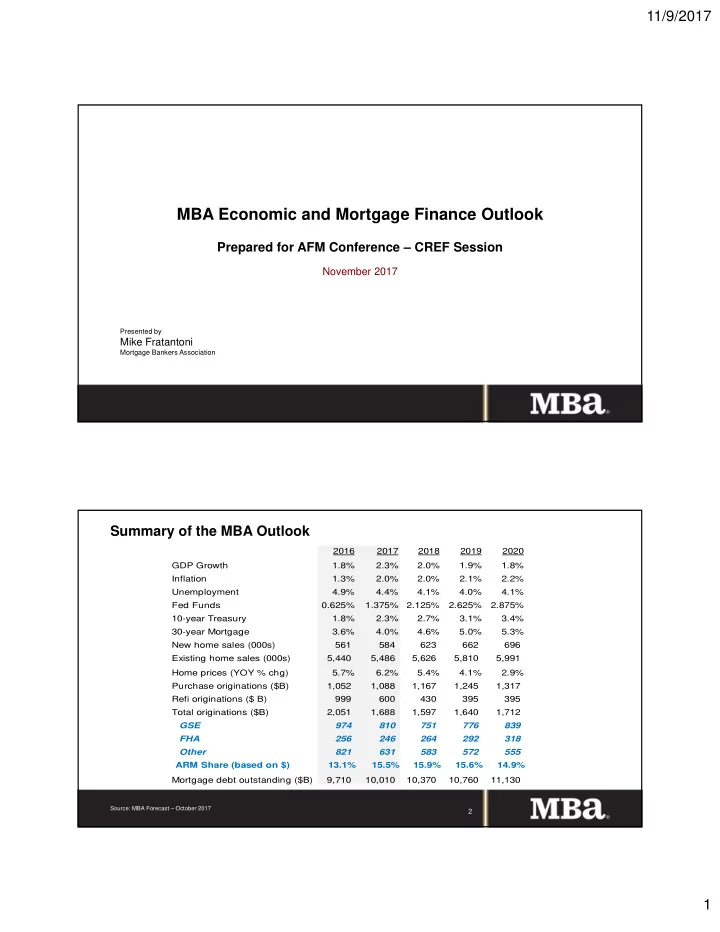

MBA Economic and Mortgage Finance Outlook

Prepared for AFM Conference – CREF Session

November 2017

Presented by

Mike Fratantoni

Mortgage Bankers Association

Summary of the MBA Outlook

Source: MBA Forecast – October 2017

2

MBA Economic and Mortgage Finance Outlook Prepared for AFM - - PDF document

11/9/2017 MBA Economic and Mortgage Finance Outlook Prepared for AFM Conference CREF Session November 2017 Presented by Mike Fratantoni Mortgage Bankers Association Summary of the MBA Outlook 2016 2017 2018 2019 2020 GDP Growth

Presented by

Mortgage Bankers Association

Source: MBA Forecast – October 2017

2

Source: BLS

3

235 284 254 265 163 (144) (42) 10 170 210 174 96 (297) (422) 88 174 179 192 250 226 187 216 232 50 207 145 210 138 208 18 261 (500) (400) (300) (200) (100)

200 300 400 Thousands of jobs

Source: NFIB

4 (5.0) ‐ 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 Jan‐86 Dec‐86 Nov‐87 Oct‐88 Sep‐89 Aug‐90 Jul‐91 Jun‐92 May‐93 Apr‐94 Mar‐95 Feb‐96 Jan‐97 Dec‐97 Nov‐98 Oct‐99 Sep‐00 Aug‐01 Jul‐02 Jun‐03 May‐04 Apr‐05 Mar‐06 Feb‐07 Jan‐08 Dec‐08 Nov‐09 Oct‐10 Sep‐11 Aug‐12 Jul‐13 Jun‐14 May‐15 Apr‐16 Mar‐17

Percent of firms with hard to fill job openings, (%, SA) Net percent of firms planning to raise compensation, (%, SA)

Source: Federal Reserve Bank of Atlanta

5 0.0 1.0 2.0 3.0 4.0 5.0 6.0

Percent

Source: BLS

6 (40.0) (30.0) (20.0) (10.0) ‐ 10.0 20.0 30.0 40.0 (4.0) (3.0) (2.0) (1.0) ‐ 1.0 2.0 3.0 4.0 Jan‐14 Feb‐14 Mar‐14 Apr‐14 May‐14 Jun‐14 Jul‐14 Aug‐14 Sep‐14 Oct‐14 Nov‐14 Dec‐14 Jan‐15 Feb‐15 Mar‐15 Apr‐15 May‐15 Jun‐15 Jul‐15 Aug‐15 Sep‐15 Oct‐15 Nov‐15 Dec‐15 Jan‐16 Feb‐16 Mar‐16 Apr‐16 May‐16 Jun‐16 Jul‐16 Aug‐16 Sep‐16 Oct‐16 Nov‐16 Dec‐16 Jan‐17 Feb‐17 Mar‐17 Apr‐17 May‐17 Jun‐17 Jul‐17 Aug‐17 Sep‐17

Motor Fuel (right axis) All Items (left axis) All Items exc Food & Energy (left axis) Shelter (left axis)

7

Source: FRED, FOMC Statement

8

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 2002‐Q4 2003‐Q2 2003‐Q4 2004‐Q2 2004‐Q4 2005‐Q2 2005‐Q4 2006‐Q2 2006‐Q4 2007‐Q2 2007‐Q4 2008‐Q2 2008‐Q4 2009‐Q2 2009‐Q4 2010‐Q2 2010‐Q4 2011‐Q2 2011‐Q4 2012‐Q2 2012‐Q4 2013‐Q2 2013‐Q4 2014‐Q2 2014‐Q4 2015‐Q2 2015‐Q4 2016‐Q2 2016‐Q4 2017‐Q2 2017‐Q4 2018‐Q2 2018‐Q4 2019‐Q2 2019‐Q4 $ Trllions

MBS US Treasuries Hypothetical path

10

11 FRBNY Bonis, Brian, Jane Ihrig, and Min Wei (2017). "Projected Evolution of the SOMA Portfolio and the 10-year Treasury Term Premium Effect," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September 22, 2017, https://doi.org/10.17016/2380- 7172.2081. Data: https://www.federalreserve.gov/econres/notes/feds-notes/projected-evolution-of-the-soma-portfolio-and-the-10-year-treasury-term- premium-effect-accessible-20170922.htm#fig1

13

Source: CBO

14

Source: Federal Reserve, Freddie Mac, MBA

15

Source: S&P

16

17

Source: Census, USPS, EIA

18 970 950 650 540 1,350 1,100 750 538 971 1,344 1,177 871 1,036 1,156 1,295 200 400 600 800 1,000 1,200 1,400 1,600 2014 2015 2016 2017 Thousands

Source: Adjusted CPS, MBA

19

Source: NAR, MBA

20 1000 2000 3000 4000 5000 6000 7000 8000 2 4 6 8 10 12 1999 1999 2000 2000 2001 2001 2002 2002 2003 2003 2004 2004 2005 2005 2006 2006 2007 2007 2008 2008 2009 2009 2010 2010 2011 2011 2012 2012 2013 2013 2014 2014 2015 2015 2016 2016 2017 2017 2018 2018 2019 2019 2020 2020 Thousands Months

Months supply of existing homes on market (Months, SA, left axis) Existing Home Sales (Ths., SAAR, right axis) Number of homes available for sale (Ths., SA, right axis) EHS Forecast (right axis)

Source: MBA Builder Applications Survey

21

Source: Census, MBA

22 200 400 600 800 1000 1200 1400 1600 1800 2000 2200 Thousands

Single Family Starts (SAAR) MF Starts (SAAR) Total Completions (SAAR)

Source: BLS, NAHB

23 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 Jan‐02 Sep‐02 May‐03 Jan‐04 Sep‐04 May‐05 Jan‐06 Sep‐06 May‐07 Jan‐08 Sep‐08 May‐09 Jan‐10 Sep‐10 May‐11 Jan‐12 Sep‐12 May‐13 Jan‐14 Sep‐14 May‐15 Jan‐16 Sep‐16 May‐17

Layoffs and Discharges Rate (12 mo. moving avg., %) Hires Rate (12 mo. moving avg., %) Job Openings Rate (12 mo. moving avg., %)

Source: FHFA, BLS

24 2.3% 6.4% 2.4% ‐10.0% ‐5.0% 0.0% 5.0% 10.0% 15.0% Q1‐83 Q1‐85 Q1‐87 Q1‐89 Q1‐91 Q1‐93 Q1‐95 Q1‐97 Q1‐99 Q1‐01 Q1‐03 Q1‐05 Q1‐07 Q1‐09 Q1‐11 Q1‐13 Q1‐15 Q1‐17 Q1‐19

ECI: Wages & Salaries: Civilian Workers (SA, Dec‐05=100) FHFA House Price Index, United States (NSA, Q1‐80=100)

25

26