SLIDE 1

Sharing some of the risk of the equity-based cyclical sector

Introduction This 3 page paper illustrates one area in which risk sharing within a defined contribution pension scheme may help to secure lower volatility and protect the capital of members invested in an equity index fund. The strategy is designed to partly solve the problem of members’ dislike of investment volatility and loss, both of which contribute uncertainty around planning for retirement. The aim is to work through a concrete example of the way risk sharing might potentially be implemented that fits with pension scheme freedoms and pension transferability in the UK. The example used here is an equity-based cyclical sector risk sharing strategy. This example has been selected because the sharing of risk can take place over about 4 years and the whole of the pension fund’s asset allocation would be managed as usual. If the goal is a smoother investment outcome, the long-run historic volatility of the strategy lies between that of Gilts and that of equities. It is worth saying that this is just one type of arrangement that may be considered by schemes post 2015, being looked at here as a means of highlighting the sorts of factors scheme designers may want to take account of. NEST is currently carrying out a comprehensive consultation of the design of any future retirement solutions for its members and is looking to gather a range of views and insights.. Extra risk from investing in the cyclical sector A look at the main moving parts of an equity index reveals that some sectors are more cyclical than

- thers. For example, retailing, information technology, industrials, materials, financials and energy

tend to trend in one direction then the other more than telecommunications, utilities, healthcare and consumer staples. This trend gives the cyclical sector higher investment volatility, making it a more

- bvious candidate to consider for sharing risk among members. For example, non-cyclical sectors, of

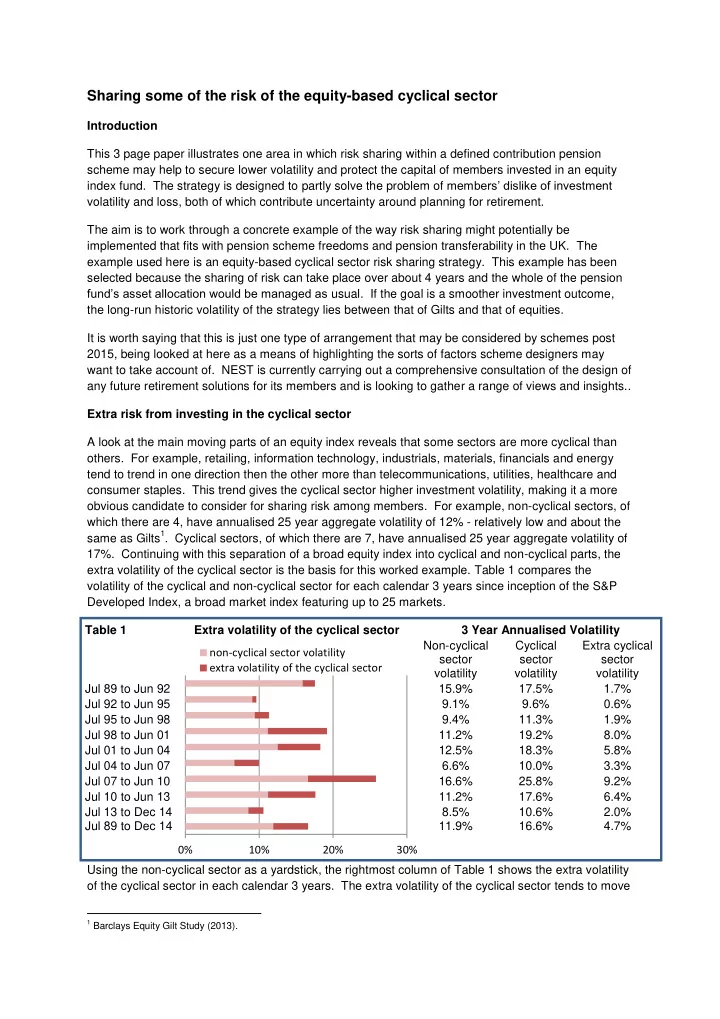

which there are 4, have annualised 25 year aggregate volatility of 12% - relatively low and about the same as Gilts1. Cyclical sectors, of which there are 7, have annualised 25 year aggregate volatility of 17%. Continuing with this separation of a broad equity index into cyclical and non-cyclical parts, the extra volatility of the cyclical sector is the basis for this worked example. Table 1 compares the volatility of the cyclical and non-cyclical sector for each calendar 3 years since inception of the S&P Developed Index, a broad market index featuring up to 25 markets. Table 1 Extra volatility of the cyclical sector 3 Year Annualised Volatility Non-cyclical sector volatility Cyclical sector volatility Extra cyclical sector volatility Jul 89 to Jun 92 15.9% 17.5% 1.7% Jul 92 to Jun 95 9.1% 9.6% 0.6% Jul 95 to Jun 98 9.4% 11.3% 1.9% Jul 98 to Jun 01 11.2% 19.2% 8.0% Jul 01 to Jun 04 12.5% 18.3% 5.8% Jul 04 to Jun 07 6.6% 10.0% 3.3% Jul 07 to Jun 10 16.6% 25.8% 9.2% Jul 10 to Jun 13 11.2% 17.6% 6.4% Jul 13 to Dec 14 8.5% 10.6% 2.0% Jul 89 to Dec 14 11.9% 16.6% 4.7% Using the non-cyclical sector as a yardstick, the rightmost column of Table 1 shows the extra volatility

- f the cyclical sector in each calendar 3 years. The extra volatility of the cyclical sector tends to move

1 Barclays Equity Gilt Study (2013).