SLIDE 1

TUTORIAL TUTORIAL -

- ABC

ABC

- Ir. Haery

- Ir. Haery Sihombing

Sihombing/IP /IP

Pensyarah Pelawat Fakulti Kejuruteraan Pembuatan Universiti Teknologi Malaysia Melaka

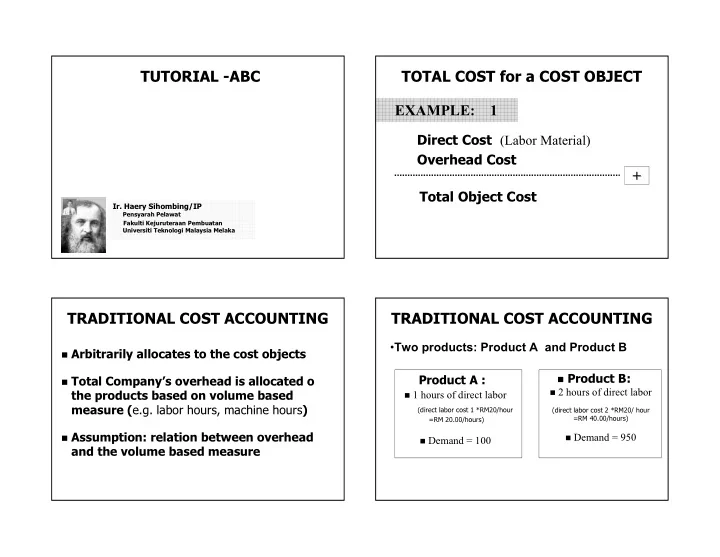

TOTAL COST for a COST OBJECT TOTAL COST for a COST OBJECT

Direct Cost Direct Cost (Labor Material) (Labor Material) Overhead Cost Overhead Cost

+ +

Total Object Cost Total Object Cost

EXAMPLE: 1 TRADITIONAL COST ACCOUNTING TRADITIONAL COST ACCOUNTING

- Arbitrarily allocates to the cost objects

Arbitrarily allocates to the cost objects

- Total Company

Total Company’ ’s overhead is allocated o s overhead is allocated o the products based on volume based the products based on volume based measure ( measure (e.g. labor hours, machine hours e.g. labor hours, machine hours) )

- Assumption: relation between overhead

Assumption: relation between overhead and the volume based measure and the volume based measure Product A : Product A :

- 1 hours of direct labor

1 hours of direct labor

(direct labor cost 1 *RM20/hour (direct labor cost 1 *RM20/hour =RM =RM 20.00/ 20.00/hours) hours)

- Demand = 100

Demand = 100

TRADITIONAL COST ACCOUNTING TRADITIONAL COST ACCOUNTING

- Product B:

Product B:

- 2 hours of direct labor

2 hours of direct labor

(direct labor cost 2 *RM20/ hour (direct labor cost 2 *RM20/ hour =RM =RM 40.00 40.00/hours) /hours)

- Demand = 950

Demand = 950

- Two products: Product A