At that time, state power supplier Eskom encountered problems with ageing plants and meeting electricity demand, necessitating power cuts to residents and businesses in the major

- cities. Country-wide rolling blackouts continue,

constraining economic growth, particularly in the energy-intensive mining and mineral processing

- sectors. Combined with South Africa’s rapid

industrialisation, these shortages have culminated in an urgent need to increase electricity generation capacity. In addition to increasing demand, the diversification of energy supply is also a key aspect of South Africa’s long-term renewable energy strategy. In its White Paper on Energy Policy 1998 and reiterated in the supplemental White Paper on Renewable Energy 2003 (White Paper), the South African Government considered a range of measures regarding the integration of renewable energies into the mainstream energy economy, and said that an increase in renewable energy capacity would provide improved

- pportunities for energy trade and would enhance

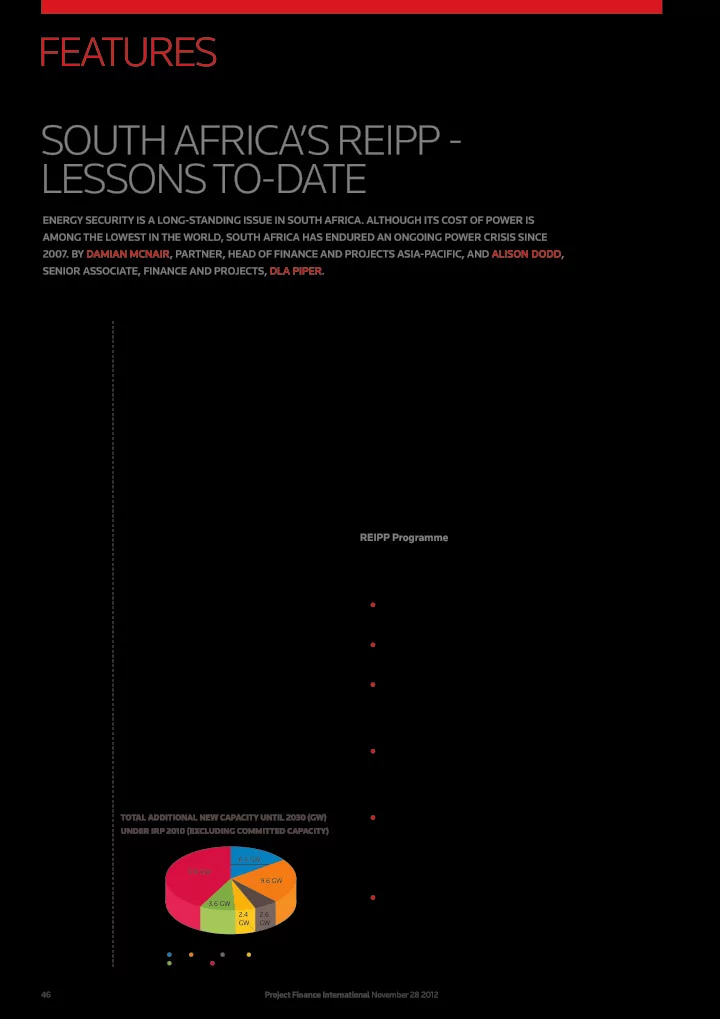

energy security by encouraging diversity of both supply sources and primary energy carriers. Under the White Paper, South Africa committed itself to a target of a 10,000GW (4%) renewable energy contribution to final energy consumption by 2013, to be produced mainly from wind, solar, biomass and small-scale hydro. In 2011 the Department of Energy (DoE) published the Integrated Resource Plan (IRP), which contemplated the addition of over 55GW of energy generation by 2030 (an increase of more than 170% on existing levels), 42% of which was to be sourced from renewable energy sources. Initially, it was assumed that the additional renewable energy capacity outlined in the IRP would be delivered by the Renewable Energy Feed-In Tariff (REFIT) Programme. Announced in 2009, the REFIT Programme proposed to provide a guaranteed tariff for electricity supply from renewable energy sources that covered the cost of generation plus a “reasonable profit”. In June 2011, the DoE announced that it would no longer proceed with the REFIT Programme and that it would instead procure the additional capacity under a programme now known as the Renewable Energy Independent Power Producers Procurement Programme (REIPP Programme).

REIPP Programme

Under the REIPP Programme, bidders submit bids to construct and operate renewable energy projects and sell power to Eskom. Key features of the REIPP Programme include:

A competitive bid process with five rounds

(phases), with selection on price and non-price criteria;

Bidders must meet minimum thresholds in

respect of economic development requirements in order for their bid to be compliant;

In addition to minimum thresholds, there is a

strong weighting on criteria relating to job creation, local content and ownership, social development, preferential procurement and management control for black South Africans;

Bidders bid the price (tariff) that will be

payable by Eskom (as buyer) pursuant to the power purchase agreement (PPA), with the price not to exceed the price cap for each technology for each phase;

Bidders required to submit the detailed heads

- f terms of material contracts, including financing

agreements and construction and operation contracts (generally an engineer, procure and construct (EPC) contract and an operating and maintenance (O&M) contract); and

Successful (preferred) bidders required to

reach financial close and commercial operation of the project within specified time-frames. The technologies comprising the REIPP Programme, and their envisaged split, are set out below in Table 1.

Project Finance International November 28 2012 46

SOUTH AFRICA’S REIPP - LESSONS TO-DATE

ENERGY SECURITY IS A LONG-STANDING ISSUE IN SOUTH AFRICA. ALTHOUGH ITS COST OF POWER IS AMONG THE LOWEST IN THE WORLD, SOUTH AFRICA HAS ENDURED AN ONGOING POWER CRISIS SINCE

- 2007. BY DAMIAN MCNAIR, PARTNER, HEAD OF FINANCE AND PROJECTS ASIA-PACIFIC, AND ALISON DODD,

SENIOR ASSOCIATE, FINANCE AND PROJECTS, DLA PIPER.

FEATURES

Coal Nuclear Hydro Gas-CCGT Peak-OCGT Renewables 15% 23% 6% 42% 9% 5% 17.8 GW 6.3 GW 9.6 GW 2.6 GW 2.4 GW 3.6 GW

TOTAL ADDITIONAL NEW CAPACITY UNTIL 2030 (GW) UNDER IRP 2010 (EXCLUDING COMMITTED CAPACITY)