SLIDE 1

8/7/2019 1

U.S. Dairy Sector at Crossroads

2019 Midsouth Ruminant Nutrition Conference Grapevine, TX August 7, 2019

- Dr. Marin Bozic

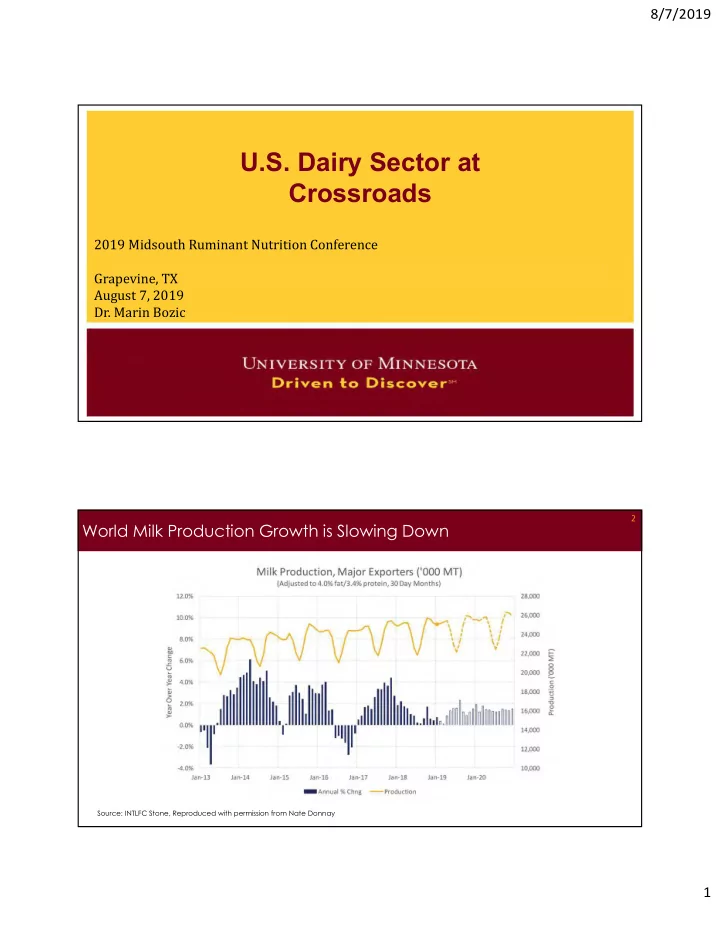

World Milk Production Growth is Slowing Down

2

Source: INTLFC Stone, Reproduced with permission from Nate Donnay