Latin Manharlal Securities Pvt Ltd

Weekender

December 30th, 2011

Index Closing Chg Chg(%)

Sensex 15454.92

- 283.78

- 1.8%

Nifty 4624.3

- 89.70

- 1.9%

Auto 8143.65

- 137.82

- 1.7%

Bankex 9153.39

- 376.47

- 4.0%

Cap Goods 8067.63

- 91.86

- 1.1%

Cons Durables 5284.33

- 43.95

- 0.8%

FMCG 4035.31

- 52.87

- 1.3%

Healthcare 5870.52 12.15 0.2% IT 5751.93 75.95 1.3% Metal 9293.17

- 238.45

- 2.5%

Oil & Gas 7529.27

- 396.88

- 5.0%

Power 1795.95

- 17.11

- 0.9%

Realty 1375.65

- 52.03

- 3.6%

World Index Closing Chg(`) Chg(%)

Dow Jones 12287.04 117.39 1.0% Nasdaq 2613.74 14.29 0.5% Hang Seng 18434.39

- 194.78

- 1.0%

Nikkei 225 8455.35 60.19 0.7% FTSE 100 5552.44 61.44 1.1% Brazil Bovespa 56754.08

- 593.79

- 1.0%

Russia RTS 1368.08

- 37.20

- 2.6%

Mexico Bolspa 37185.73 118.96 0.3% Singapore Strait 2646.35

- 30.12

- 1.1%

* As on Friday 4pm

Top Gainers Closing Chg(`) Chg(%)

Redington (India) Lt 81.75 11.5 16.4% GMR Infrastructure L 21.9 2.3 11.7% Jaypee Infratech Ltd 39.85 3.2 8.7% MMTC Ltd. 537.9 40.7 8.2% Cadila Healthcar 705 47.4 7.2%

* As on 30th Dec,11

Top Losers Closing Chg(`) Chg(%)

United Spirits Ltd. 491.15

- 102.85

- 17.3%

- Guj. Fluorochemi

345

- 40.7

- 10.6%

Central Bank 65.95

- 7.75

- 10.5%

Oriental Bank of 196.75

- 21.8

- 10.0%

Bank of India 266.3

- 26.45

- 9.0%

* As on 30th Dec,11

Metal Closing Chg Chg(%)

Gold($/oz) 1571.71

- 34.64

- 2.2%

Silver($/oz) 27.89

- 1.23

- 4.2%

Aluminium($/MT) 1974.00

- 31.00

- 1.5%

Copper($/MT) 7413.75

- 117.75

- 1.6%

Lead($/MT) 1975.50

- 4.00

- 0.2%

Zinc($/MT) 1815.75

- 20.75

- 1.1%

* As on Friday 4pm

Date DII(cash) FII(Cash) FII(FO)

26-Dec-11 53.1 272 113.43 27-Dec-11 6.7 153.7 214.31 28-Dec-11

- 67.8

363.7 81.44 29-Dec-11 NA 169.7

- 1015.82

30-Dec-11 NA NA NA NA- Not Available

ADR's Closing * Chg($) Chg(%)

Infosys 51.33 0.26 0.5% ICICI Bank 26.26

- 0.83

- 3.1%

HDFC BANK 25.86

- 0.31

- 1.2%

Tata Motors 16.89

- 0.57

- 3.3%

Wipro 10.11 0.09 0.9%

* As on Thursday

SNAP SHOT

During the week ended 30th December 2011, key benchmark indices closed negative as bears tightened their grip on the market in the last week of the CY2011. Expectations of weak Q3 corporate earnings weighed on the domestic bourses as the key benchmark indices dropped for the fourth day in a row. Recent media reports that Indian and Mauritian tax officials have begun talks on revising the double taxation avoidance pact between the two countries also weighed on sentiment as it could adversely impact foreign fund flow into Indian equity market. ~40% of FIIs inflows and ~42% of the FDI in India are routed through Mauritius. While short-term capital gains are taxed at 15% in India, they are exempted in Mauritius. Several companies take advantage of the double taxation avoidance pact between the two countries and escape paying taxes in both the countries. A weak rupee added to investors' woes. The currency slid over 15% this year, the worst performance among Asian currencies,

- n concern Europe's debt crisis will slow global growth and damp

demand for emerging-market assets. FIIs sold shares worth a hefty `1015.82 Crs on 29th Dec’11. Automobile and cement stocks will be in focus in next week as companies from these two sectors start unveiling monthly sales volumes data for December 2011 from 1 January 2012. Auto stocks will also hog limelight ahead of the commencement of New Delhi Auto Expo 2012 on 7th January 2012. The next major trigger for the market is 3Q12E corporate earnings, which will start tricking from 2nd week of January

- 2012. The focus will be on guidance from the company

managements on outlook for the remaining part of the year and for the next year. Analysts expect weak Q3 December 2011 results due to lower volume growth in a slowing economy, higher raw material costs and higher interest charges.

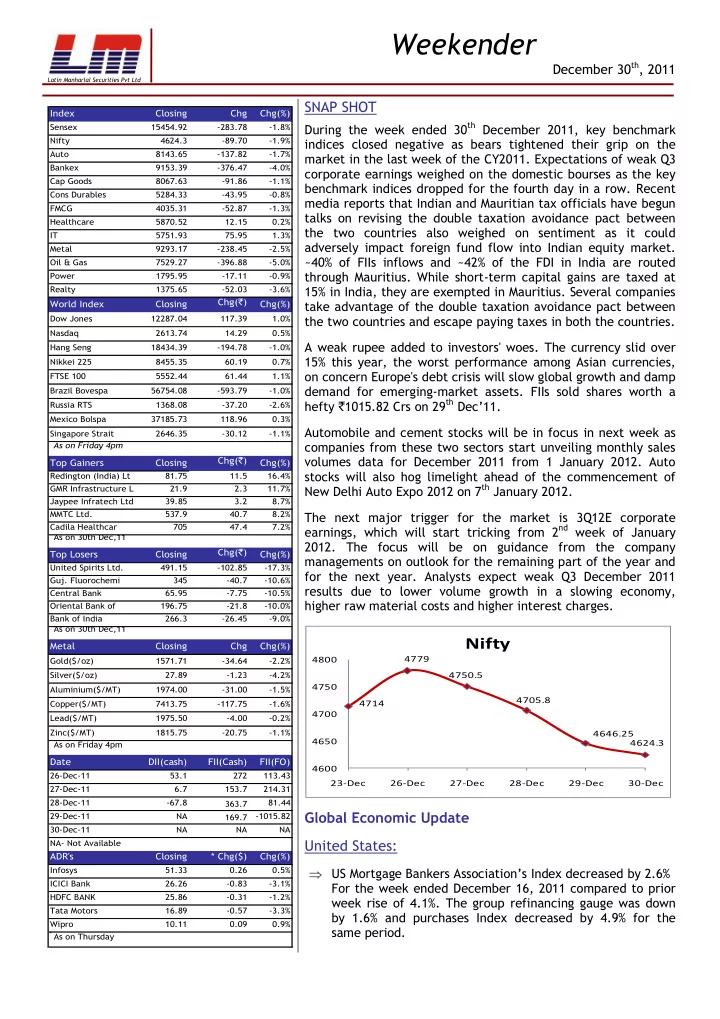

4714 4779 4750.5 4705.8 4646.25 4624.3 4600 4650 4700 4750 4800 23-Dec 26-Dec 27-Dec 28-Dec 29-Dec 30-Dec

Nifty

Global Economic Update United States:

US Mortgage Bankers Association’s Index decreased by 2.6% For the week ended December 16, 2011 compared to prior week rise of 4.1%. The group refinancing gauge was down by 1.6% and purchases Index decreased by 4.9% for the same period.