SLIDE 4 4

7

50,000 100,000 150,000 200,000 250,000 300,000 350,000 2001 2002 2003 2004 2005

New customers and cold drink equipment driving product availability

15% increase in active customers in 2005 19% increase in cold drink coolers in 2005

Cold drink coolers Active customers

100,000 200,000 300,000 400,000 500,000 600,000 700,000 2001 2002 2003 2004 2005

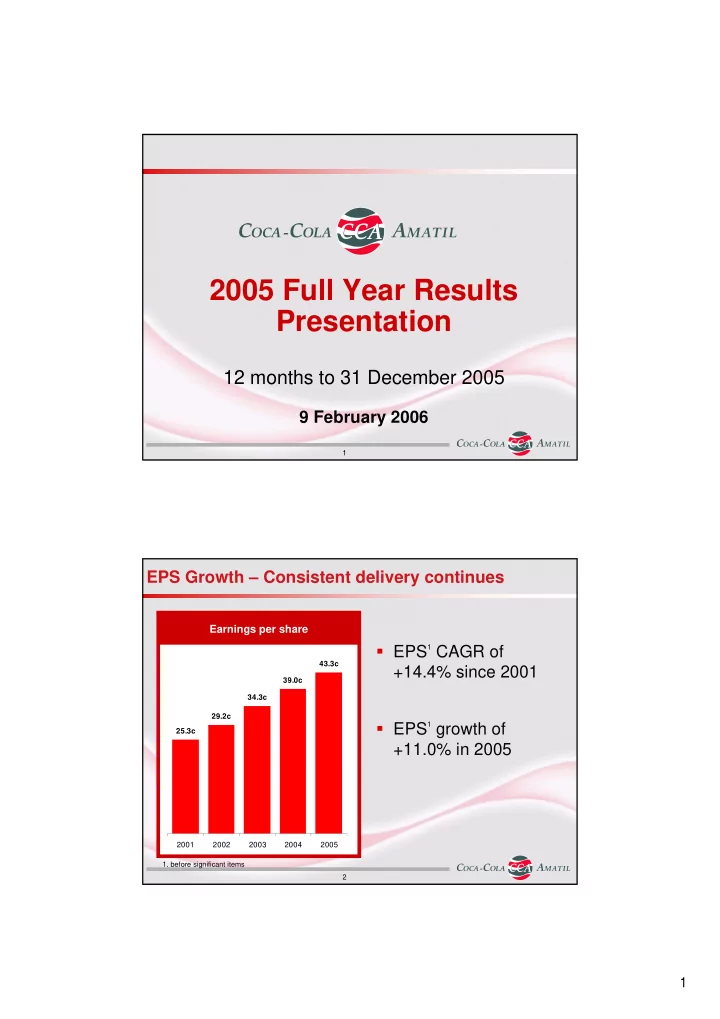

8

Group EBIT

1 10.1% to $570.6m

Beverage EBIT margin a healthy 15.5% Food EBIT margin 13.0% (10 months)

Standout result from Indonesia with 49.6% local currency EBIT growth

32.4% to $42.9m Indonesia & PNG1

Result better than expectations with strong local currency revenue growth in H2 of 10.2%

EBIT loss of $6.6m South Korea1

Solid earnings result despite an intensifying competitive environment

$45.7m (10 months) SPC Ardmona

Competitive trading conditions in New Zealand lead to under-recovery of COGS

12.1% to $72.0m Pacific

EBIT margin maintained in a competitive market

5.3% to $455.5m Australia

Solid group performance continues

- 1. before significant items